<Back to Index>

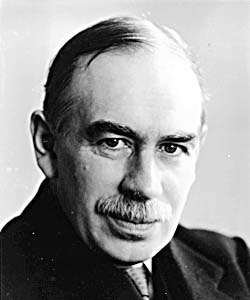

- Political Economist John Maynard Keynes, 1883

- Poet Federico García Lorca, 1898

- General José Doroteo Arango Arámbula (Pancho Villa), 1878

John Maynard Keynes, 1st Baron Keynes, CB (5 June 1883 – 21 April 1946) was a British economist whose ideas have profoundly affected modern macroeconomics and social liberalism, both in theory and practice. He advocated interventionist economic policy, by which governments would use fiscal and monetary measures to mitigate the adverse effects of business cycles, economic recessions, and depressions. His ideas are the basis for the school of thought known as Keynesian economics, and its various offshoots.

In the 1930s, Keynes spearheaded a revolution in economic thinking, overturning the older ideas of neoclassical economics that

held that free markets would automatically provide full employment as

long as workers were flexible in their wage demands. Following the

outbreak of World War II,

Keynes's ideas concerning economic policy were adopted by leading

Western economies. During the 1950s and 1960s, the success of Keynesian

economics was so resounding that almost all capitalist governments

adopted its policy recommendations. In 1999, Time magazine included Keynes in their list of the 100 most important and influential people of the 20th century, commenting that: "His radical idea that governments should spend money they don't have may have saved capitalism". Keynes's influence waned in the 1970s, partly as a result of problems that began to afflict the Anglo-American economies from the start of the decade, and partly due to critiques from Milton Friedman and

other economists who were pessimistic about the ability of governments

to regulate the business cycle with fiscal policy. However, the advent

of the global financial crisis in 2007 has caused a resurgence in Keynesian thought. Keynesian economics has provided the theoretical underpinning for the plans of President Barack Obama of the United States, Prime Minister Gordon Brown of the United Kingdom, and other global leaders to ease the economic recession. Keynes is widely considered the father of modern macroeconomics, and by various commentators such as economist John Sloman, the most influential economist of the 20th century. In addition to being an economist, Keynes was also a civil servant, a patron of the arts, a director of the Bank of England, an advisor to several charitable trusts, a writer, a private investor, an art collector, and a farmer. Keynes was bisexual, openly acknowledging the homosexual relationships he had with other men. In 1925, he married the Russian ballerina Lydia Lopokova. Of towering stature, Keynes stood at six foot, six inches. John Maynard Keynes was born in Cambridge to a middle-class family. His father, John Neville Keynes, was a lecturer at Cambridge University and his mother Florence Ada Keynes a local social reformer. Keynes was the first born, and was followed by two more children - Geoffrey Keynes in 1887 and Margaret Neville Keynes in 1890. According to economist and biographer Robert Skidelsky,

Keynes' parents were loving and attentive, but not smotheringly so.

They remained in the same house throughout their lives, where the

children were always welcome to return. Keynes would receive

considerable support from his father; including expert coaching to help

him pass his scholarship exams and financial help both as a young man

and when he was nearly wiped out at the onset of Great Depression in

1929. Keynes' mother made her children's interests her own, and

according to Skidelsky, "because she could grow up with her children,

they never outgrew home". Keynes had his early education at home and in kindergarten. He attended St Faith's preparatory school as

a day pupil from 1892-1897. Teachers described Keynes as brilliant, but

on occasion, careless and lacking in determination. His health was

often poor during this period, leading to several long absences. Keynes won a scholarship to study at Eton,

where he displayed talent in a wide range of subjects, particularly

mathematics, classics and history. Despite his middle-class background,

Keynes mixed easily with upper-class pupils. In 1902 Keynes left Eton

for King's College, Cambridge, to study mathematics. The famous Alfred Marshall begged Keynes to become an economist, although Keynes's own inclinations drew him towards philosophy – especially the ethical system of G.E. Moore. Keynes was an active member of the semi-secretive Cambridge Apostles society,

a debating club largely reserved for the brightest students. Like many

members, Keynes retained a bond to the club after graduating and

continued to attend occasional meetings throughout his life. Before

leaving Cambridge, Keynes became the President of the Cambridge University Liberal Club.

In May 1904 he received a first class B.A. in mathematics. Aside from a

few months spent on holidays with family and friends, Keynes continued

to involve himself with the university over the next two years. He took

part in debates, further studied philosophy and attended economics

lectures informally as a graduate student. He also studied for his 1905 Tripos and 1906 Civil Service exams. The economist Harry Johnson wrote that the optimism imparted by Keynes's early life is key to understanding his later thinking. Keynes

was always confident he could find a solution to whatever problem he

turned his attention to, and retained a lasting faith in the ability of

government officials to do good. Keynes

optimism was also cultural, in two senses – he was of the last

generation raised by an empire still at the height of its power, in its

own eyes and by much of the world (at least outwardly) seen as

preeminent in both power and benevolence. Keynes was also of the last

generation who felt entitled to govern by culture, rather than by

expertise. According to Skidelsky, the sense of cultural unity current

in Britain from the 19th century to the end of World War I, provided

the well educated a framework with which to set various spheres of

knowledge in relation to each other and to life, enabling them to

confidently draw from different fields when addressing practical

problems.

Keynes's Civil Service career began in October 1906, as a clerk in the India Office. He enjoyed his work at first, but by 1908 had become bored and resigned his position to return to Cambridge and work on probability theory, at first privately funded only by two Dons at the university – his father and the economist Arthur Pigou. In 1909 Keynes's published his first professional economics article in the Economics Journal, about the effect of a recent global economic downturn on India. Also

in 1909, Keynes accepted a lectureship in economics funded personally

by Alfred Marshall. Keynes's earnings rose further as he began to take

on pupils for private tuition, and on being elected a fellow. In 1911

Keynes was made editor of the Economic Journal. By 1913 he had published his first book, Indian Currency and Finance. He was then appointed to the Royal Commission on Indian Currency and Finance – the same topic as his book – where Keynes showed considerable talent at applying economic theory to practical problems. The British Government called on Keynes's expertise during the First World War.

While he did not formally re-join the civil service in 1914, Keynes

travelled to London at the government's request a few days before

hostilities started. Bankers had been pushing for the suspension of specie payments – the convertibility of bank notes into gold – but with Keynes's help the Chancellor of the Exchequer (then Lloyd George)

was persuaded that this would be a bad idea, as it would hurt the

future reputation of the city if payments were suspended before

absolutely necessary. In January 1915 Keynes took up an official government position at the Treasury.

Among his responsibilities were the design of terms of credit between

Britain and its continental allies during the war, and the acquisition

of scarce currencies. According to economist Robert Lekachman,

Keynes's "nerve and mastery became legendary" due to his performance of

these duties, as in the case where he managed to assemble — with

difficulty — a small supply of Spanish pesetas.

The secretary of the Treasury was delighted to hear Keynes had amassed

enough to provide a temporary solution for the British Government. But

Keynes did not hand the pesetas over, he sold them all to break the

market: his boldness paid off, as pesetas then became much less scarce

and expensive. In the 1917 King's Birthday Honours, Keynes was appointed Companion of the Order of the Bath for his wartime work, and

his success led to the appointment that would have a huge effect on

Keynes's life and career; Keynes was appointed financial representative

for the Treasury to the 1919 Versailles peace conference. He was also appointed Officer of the Belgian Order of Leopold. Keynes's experience at Versailles was

influential in shaping his future outlook, yet it was not a successful

one for him. Keynes's main interest had been in trying to prevent

Germany's compensation payments being set so high it would traumatize

innocent German people, damage the nation's ability to pay and sharply

limit her ability to buy exports from other countries - thus hurting

not just Germany's own economy but that of the wider world.

Unfortunately for Keynes, conservative powers in the coalition that

emerged from the 1918 coupon election were

able to ensure both Keynes himself and the Treasury were largely

excluded from formal high-level talks concerning reparations. Their

place was taken by the Heavenly Twins - the Judge Lord Sumner and the Banker Lord Cunliffe whose

nickname derived from the "astronomically" high war compensation they

wanted to demand from Germany. Keynes was forced to try to exert

influence mostly from behind the scenes. The three principal players at Versailles were Britain's Lloyd George, France's Clemenceau and America's President Wilson. It

was only Lloyd George to whom Keynes had much direct access; until the

1918 election he had some sympathy with Keynes's view but while

campaigning had found his speeches were only well-received by the

public if he promised to harshly punish Germany, and had therefore

committed to extracting high payments. Lloyd George did however win

some loyalty from Keynes with his actions at the Paris conference by

intervening against the French to ensure the dispatch of much-needed

food supplies to German civilians. Clemenceau also pushed for high

reparations; generally France argued for an even more severe settlement

than Britain. Wilson initially favoured relatively lenient treatment of

Germany – he feared too harsh conditions could foment the rise of

extremism, and wanted Germany to be left sufficient capital to pay for

imports. To Keynes's dismay, Lloyd George and Clemenceau were able to

pressure Wilson to agree to very high repayments being imposed. Towards

the end of the conference, Keynes came up with a plan that he argued

would not only help Germany and other impoverished central European

powers but also be good for the world economy as a whole. It involved

the writing down of war debts which would have the effect of increasing

international trade all round. Lloyd George agreed it might be

acceptable to the British electorate. However America was against it,

the US then being the largest creditor and by this time Wilson had

started to believe in the merits of a harsh peace as a warning to

future aggressors. So despite his best efforts, the end result of the

conference was a treaty which disgusted Keynes both on moral and

economic grounds, and led to his resignation from the Treasury. Keynes's analyses on the predicted damaging effects of the treaty appeared in the highly influential book, The Economic Consequences of the Peace,

published in 1919. This work has been described as Keynes's best book,

where he was able to bring all his gifts to bear - his passion as well

as his skill as an economist. In addition to economic analysis, the

book contained pleas to the reader's sense of compassion: Also

present was striking imagery such as "...that year by year Germany must

be kept impoverished and her children starved and crippled..." along

with bold predictions which were later justified by events: Keynes's predictions of disaster were borne out when the German economy suffered the hyperinflation of 1923, and again by the collapse of the Weimar Republic and the outbreak of World War II. Only a fraction of reparations were ever paid. The Economic Consequences of the Peace gained

Keynes international fame, but also caused him to be regarded as

anti-establishment – it was not until after the outbreak of World War

II that Keynes was offered a directorship of a major British Bank, or

an acceptable offer to return to government with a formal job. Keynes

was still able to influence policy making however – through his network

of contacts, his published works and by serving on government

committees, including attending high-level policy meetings as a

consultant. Keynes had completed his Treatise on Probability before the war, but published it in 1921. The work was a notable contribution to the philosophical and mathematical underpinnings of probability theory, championing the important view that probabilities were no more or less than truth values intermediate

between simple truth and falsity. Keynes developed the first

upper-lower probabilistic interval approach to probability in chapters

15 and 17 of this book, as well as having developed the first decision

weight approach with his conventional coefficient of risk and weight. In addition to his academic work, the 1920s saw Keynes

active as a journalist selling his work internationally and working in

London as a financial consultant. In 1924 Keynes wrote an obituary for

his former tutor Alfred Marshall which Schumpeter called "the most brilliant life of a man of science I have ever read." Marshall's widow was "entranced" by the memorial, while Lytton Strachey rated it as one of Keynes's "best works". In 1922 Keynes continued to advocate reduction of German reparations with A Revision of the Treaty. He attacked the post World War I deflation policies with A Tract on Monetary Reform in 1923 –

a trenchant argument that countries should target stability of domestic

prices, avoiding deflation even at the cost of allowing their currency

to depreciate. The 1920s saw high unemployment in Britain even before

the outbreak of the Great Depression - in addition to advocating

depreciating the currency as a way to boost jobs by making British

exports more affordable, Keynes was from 1924 to start recommending a

fiscal response to unemployment by means of government spending on

public works. During

the 20's Keynes' pro stimulus views had only limited effect on policy

makers and mainstream academic opinion - according to Minsky one reason

was that at this time his theoretical justification was "muddled". The Tract had

also called for an end to the gold standard. Keynes advised it was no

longer a net benefit for countries such as Britain to participate in

the gold standard, as it ran counter to the need for domestic policy

autonomy. It could force countries to pursue deflationary policies at

exactly the time when expansionary measures were called for to address

rising unemployment. The Treasury and Bank of England were still in

favor of the gold standard and in 1925 they were able to convince the

then Chancellor Winston Churchill to re-establish it, which had a depressing effect on British industry. Keynes responded by writing The Economic Consequences of Mr. Churchill and continued to argue against the gold standard until Britain finally abandoned it in 1931.

Keynes had begun a theoretical work to examine the relationship between unemployment, money and prices back in the 1920s. The work, Treatise on Money,

was published in 1930 in two volumes. A central idea of the work was

that if the amount of money being saved exceeds the amount being

invested – which can happen if interest rates are too high – then

unemployment will rise. This is in part a result of people not wanting

to spend too high a proportion of what employers pay out, making it

difficult, in aggregate, for employers to make a profit. At the height

of the Great Depression, in 1933, Keynes published The Means to Prosperity,

which contained specific policy recommendations for tackling

unemployment in a global recession, chiefly counter cyclical public

spending. The Means to Prosperity contains one of the first mentions of the multiplier effect.

While it was addressed chiefly to the British Government, it also

contained advice for other nations affected by the global recession. A

copy was sent to the newly elected President Roosevelt and

other world leaders. The work was taken seriously by both the American

and British governments, and according to Skidelsky, helped pave the

way for the later acceptance of Keynesian ideas, though it had little

immediate practical influence. In the 1933 London Economic Conference opinions remained too diverse for a unified course of action to be agreed upon. Keynesian-like

policies were adopted by Sweden and Germany, but Sweden was seen as too

small to command much attention, and Keynes was deliberately silent

about the successful efforts of Germany as he was dismayed by their

imperialist ambitions and their treatment of Jews. Apart

from Great Britain, Keynes attention was primarily focused on the

United States. In 1931, he received considerable support for his views

on counter-cyclical public spending in Chicago, then America's foremost

centre for economic views alternative to the mainstream. However,

orthodox economic opinion remained generally hostile regarding fiscal

intervention to mitigate the depression, until just before the outbreak

of war. In late 1933 Keynes was persuaded by Felix Frankfurter to

address President Roosevelt directly, which he did by letters and face

to face in 1934, after which the two men spoke highly of each other. However

according to Skidelsky, the consensus is that Keynes efforts only began

to have a more than marginal influence on US economic policy after 1939. Keynes's magnum opus, the General Theory of Employment, Interest and Money was published in 1936. It was researched and indexed by one of Keynes's favourite students, later the economist David Bensusan-Butt. The work served as a theoretical justification for the interventionist policies Keynes favored for tackling a recession. The General Theory challenged the earlier neo-classical economic paradigm,

which had held that provided it was unfettered by government

interference, the market would naturally establish full employment

equilibrium. In doing so Keynes was partly setting himself against his

former teachers Marshal and Pigou. Keynes believed the classical theory

was a "special case" that applied only to the particular conditions

present in the 19th century, his own theory being the general one.

Classical economists had believed in Say's Law, which, simply put, states that "supply creates its own demand",

and that in a free market workers would always be willing to lower

their wages to a level where employers could profitably offer them

jobs. An innovation from Keynes was the concept of price stickiness –

the recognition that in reality workers often refuse to lower their

wage demands even in cases where a classical economist might argue it

is rational for them to do so. Due in part to price stickiness, it was

established that the interaction of "aggregate demand" and "aggregate

supply" may lead to stable unemployment equilibria – and in those

cases, it is the state, and not the market, that economies must depend

on for their salvation. The General Theory argues that demand, not supply, is the key variable governing the overall level of economic activity. Aggregate demand,

which equals total un-hoarded income in a society, is defined by the

sum of consumption and investment. In a state of unemployment and

unused production capacity, one can only enhance employment and total income by first increasing

expenditures for either consumption or investment. Without government

intervention to increase expenditure, an economy can remain trapped in

a low employment equilibrium – the demonstration of this possibility

has been described as the revolutionary formal achievement of the work. The book advocated activist economic policy by government to stimulate demand in times of high unemployment, for example by spending on public works. The General Theory is often viewed as the foundation of modern macroeconomics. Historians agree that Keynes influenced U.S. president Roosevelt's New Deal,

but disagree as to what extent. Deficit spending of the sort the New

Deal began in 1938 had previously been called "pump priming" and had

been endorsed by President Herbert Hoover. Few senior American economists agreed with Keynes through most of the 1930s. Yet his ideas were soon to achieve widespread acceptance, with eminent American professors such as Alvin Hansen agreeing with the General Theory before the outbreak of World War II. Keynes's himself had only limited participation in the theoretical debates that followed the publication of the General Theory as he suffered a heart attack in 1937, requiring him to take long periods of rest. Hyman Minsky and other post-Keynesian economists have

argued that as a result of this, Keynes's ideas were diluted by those

keen to compromise with classical economists or to render his concepts

with mathematical models like the IS/LM model (which they argue, distort Keynes's ideas). Keynes

began to recover in 1939, but for the rest of his life his professional

energies were largely directed towards the practical side of economics

– the problems of ensuring optimum allocation of resources for the War

efforts, post-War negotiations with America, and the new international

financial order that was presented at Bretton Woods. During World War II, Keynes argued in How to Pay for the War, published in 1940, that the war effort should be largely financed by higher taxation and especially by compulsory saving (essentially workers loaning money to the government), rather than deficit spending, in order to avoid inflation.

Compulsory saving would act to dampen domestic demand, assist in

channelling additional output towards the war efforts, would be fairer

than punitive taxation and would have the advantage of helping to avoid

a post war slump by boosting demand once workers were allowed to

withdraw their savings. In September 1941 he was proposed to fill a

vacancy in the Court of Directors of the Bank of England, and subsequently carried out a full term from the following April. In June 1942, Keynes was rewarded for his service with an hereditary peerage in the King's Birthday Honours. On 7 July his title was gazetted as Baron Keynes, of Tilton in the County of Sussex, and he took his seat in the House of Lords on the Liberal Party benches.

As Allied victory began to look certain, Keynes was heavily involved,

as leader of the British delegation and chairman of the World Bank commission, in the mid-1944 negotiations that established the Bretton Woods system. The Keynes-plan, concerning an international clearing-union argued for a radical system for the management of currencies. He proposed the creation of a common world unit of currency, the Bancor and of new global institutions — a world central bank and the International Clearing Union.

Keynes envisaged these institutions managing an international trade and

payments system with strong incentives for countries to avoid

substantial trade deficits or surpluses. The USA's greater negotiating

strength, however, meant that the final outcomes accorded more closely

to the less radical plans of Harry Dexter White. According to US economist Brad Delong, on almost every point where he was overruled by the Americans, Keynes was later proved correct by events. The two new institutions, later known as the World Bank and IMF,

were founded as a compromise that primarily reflected the American

vision. There would be no incentives for states to avoid a large trade

surplus, instead the burden for correcting a trade imbalance would

continue to fall just on the deficit countries, which Keynes had argued

were least able to address the problem without inflicting economic

hardship on their populations. Yet Keynes was still pleased when

accepting the final agreement, saying that if the institutions stayed

true to their founding principles, "the brotherhood of man will have

become more than a phrase." From the end of the Great Depression to

the mid-1970s, Keynes provided the main inspiration for economic policy

makers in Europe, America and much of the rest of the world. While

economists and policy makers had become increasingly won over to

Keynes's way of thinking in the mid and late 1930s, it was only after

the outbreak of World War II that governments started to borrow money

for spending on a scale sufficient to eliminate unemployment. According

to economist John Kenneth Galbraith,

then a US government official charged with controlling inflation, "one

could not have had a better demonstration of the Keynesian ideas." The Keynesian Revolution was associated with the rise of modern liberalism in the West during the post-war period. Keynesian ideas became so popular that some scholars point to Keynes as representing the ideals of modern liberalism, like Adam Smith represented the ideals of classical liberalism. After the war Winston Churchill attempted to check the rise of Keynesian policy making in Great Britain. He had been influenced by Hayek's 1944 book The Road to Serfdom, and used rhetoric critical of the mixed economy in his 1945 election campaign. Despite his popularity as a war hero Churchill suffered a landslide defeat to Clement Attlee whose government's economic policy continued to be influenced by Keynes's ideas. In the late 1930s and 1940s, economists (notably John Hicks, Franco Modigliani, and Paul Samuelson), attempted to interpret and formalize Keynes' writings in terms of formal mathematical models. In a process termed "the neoclassical synthesis", they combined Keynesian analysis with neo-classical economics to produce Neo-Keynesian economics, which came to dominate mainstream macroeconomic thought for the next 40 years. By

the 1950s, Keynesian policies were adopted by almost the entire

developed world and similar measures for a mixed economy were used by

many developing nations. By then, Keynes's views on the economy had

become mainstream in the world's universities. Throughout the 1950s and

1960s, Europe, the United States and Japan enjoyed considerably lower

unemployment and higher growth than they have had before or since.

Professor Gordon Fletcher has written that the fifties and sixties,

when Keynes' influence was at its peak, appear in retrospect as a Golden Age of Capitalism. In late 1965 Time magazine ran a cover article with the title inspired by a possibly tongue-in-cheek comment from Milton Friedman, a comment later echoed by U.S. President Richard Nixon, that "We are all Keynesians now".

The article described the exceptionally favourable economic conditions

then prevailing, and reported that "Washington's economic managers

scaled these heights by their adherence to Keynes's central theme: the

modern capitalist economy does not automatically work at top

efficiency, but can be raised to that level by the intervention and

influence of the government." The article also states that Keynes was

one of the three most important economists who ever lived, and that his General Theory was more influential than the magna opera of other famous economists, like Smith's The Wealth of Nations. Keynesian

economics were officially discarded by the British Government in 1979,

but forces had began to gather against Keynes's ideas over 30 years

earlier. Friedrich von Hayek had formed the Mont Pelerin Society in

1947, with the explicit intention of nurturing intellectual currents to

one day displace Keynesianism and other collectivist influences. Its

members included Austrian School founder Ludwig von Mises along

with the then young Milton Friedman. Initially the society had little

impact on the wider world - Hayek was to say it was as if Keynes had

been raised to sainthood after his death and that people refused to

allow his work to be questioned. Friedman

however began to emerge as a formidable critic of Keynesian economics

from the mid 1950s, and especially after his 1963 publication of A Monetary History of the United States. On

the practical side of economic life, big government had appeared to be

firmly entrenched in the 1950s but the balance began to shift towards

private power in the sixties. Keynes had written against the folly of

allowing "decadent and selfish" speculator and financiers the kind of

influence they had enjoyed after World War I. For two decades after

World War II public opinion was strongly against private speculators,

the disparaging label Gnomes of Zürich being

typical of how they were described during this period. International

speculation was severely restricted by the capital controls in place

after Bretton Woods. Journalists Larry Elliott and Dan Atkinson say

1968 was a pivotal year when power shifted in the favour of private

agents such as currency speculators. They pick out a key 1968 event as

being when America suspended the conversion of the dollar into gold

except on request of foreign governments, which they identify as when

the Bretton Woods system first began to break down. Intellectually,

attacks against Keynes's ideas had begun to gain significant acceptance

from the early 1970s as they were able to make a credible case that

Keynesian models no longer reflected economic reality. Keynes himself

had included few formulæ and no explicit mathematical models in

his General Theory. For commentators such as economist Hyman Minsky,

Keynes's limited use of mathematics was partly the result of his

scepticism about whether phenomena as inherently uncertain as economic

activity could ever be adequately captured by mathematical models.

Nevertheless, many models were developed by Keynesian economists, with

a famous example being the Phillips curve which

predicted an inverse relationship between unemployment and inflation.

It implied that unemployment could be reduced by government stimulus

with a calculable cost to inflation. In 1968 Milton Friedman published

a paper arguing that the fixed relationship implied by the Philips

curve did not exist. Friedman

suggested that sustained Keynesian policies could lead to both

unemployment and inflation rising at once — a phenomenon that soon became

known as stagflation.

In the early 1970s stagflation appeared in both the US and Britain just

as Friedman had predicted, with economic conditions deteriorating

further after the 1973 oil crisis.

Aided by the prestige gained from his successful forecast, Friedman led

increasingly successful attacks against the Keynesian consensus,

convincing not only academics and politicians but also much of the

general public with his radio and television broadcasts. The academic

credibility of Keynesian economics was further undermined by additional

criticism from other Monetarists trained in the Chicago school of economics, by the Lucas Critique and by attacks from Hayek's Austrian School. So successful were these attacks that by 1980 Robert Lucas was saying economists would often take offence if described as Keynesians. Keynesian

principles fared increasingly poorly on the practical side of

economics — by 1979 they had been displaced by Monetarism as the primary

influence on Anglo-American economic policy. However

many officials on both sides of the Atlantic retained a preference for

Keynes, and in 1984 the Federal Reserve officially discarded

monetarism, after which Keynesian principles made a partial comeback as

an influence on policy making. Not

all academics accepted the criticism against Keynes — Minsky has argued

that Keynesian economics had been debased by excessive mixing with

neo-classical ideas from the 1950s, and that it was unfortunate the

branch of economics had even continued to be called "Keynesian". The American Prospect have

argued it was not so much excessive Keynesian activism that caused the

economic problems of the 1970s but the breakdown of the Bretton Woods

system of capital controls, which allowed capital flight from countries the markets viewed as excessively Keynesian or socially progressive. Historian

Peter Pugh has stated a key cause of the economic problems afflicting

America in 1970s was the refusal to raise taxes to finance the Vietnam War, which was against Keynesian advice. A

more typical response was to accept some elements of the criticisms

while refining Keynesian economic theories to defend them against

arguments that would invalidate the whole Keynesian framework — the

resulting body of work largely composing New Keynesian economics. In 1992 Alan Blinder was

writing about a "Keynesian Restoration" as work based on Keynes's ideas

had to some extent become fashionable once again in academia, though in

the mainstream it was highly synthesized with Monetarism and other

neo-classical thinking. In the world of policy making, free-market

influences broadly sympathetic to Monetarism remained very strong at

government level — in powerful normative institutions like the World

Bank, IMF and US Treasury, and in prominent opinion-forming media such

as the Financial Times and the Economist. The Financial crisis of 2007–2010 led to public skepticism about the free market consensus even from some on the economic right. In March 2008, Martin Wolf, chief economics commentator at the Financial Times, announced the death of the dream of global free-market capitalism, and quoted Josef Ackermann, chief executive of Deutsche Bank, as saying "I no longer believe in the market's self-healing power." In the same month macroeconomist James K. Galbraith used

the 25th Annual Milton Friedman Distinguished Lecture to launch a

sweeping attack against the consensus for monetarist economics and

argued that Keynesian economics were far more relevant for tackling the

emerging crises. Economist Robert Shiller had begun advocating robust government intervention to tackle the financial crises, specifically citing Keynes. Nobel laureate Paul Krugman also actively argued the case for vigorous Keynesian intervention in the economy in his columns for the New York Times. Other prominent economists arguing for Keynesian government intervention to mitigate the financial crisis include George Akerlof, Brad Delong, Robert Reich, and Joseph Stiglitz. Newspapers and other media have also cited work relating to Keynes by Hyman Minsky, Robert Skidelsky, Donald Markwell and Axel Leijonhufvud. A

series of major bail-outs were pursued during the financial crisis,

starting on 7 September with the announcement that the U.S. government

was to nationalize the two government-sponsored enterprises which oversaw most of the U.S. subprime mortgage market — Fannie Mae and Freddie Mac. In October, the British Chancellor of the Exchequer referred

to Keynes as he announced plans for substantial fiscal stimulus to head

off the worst effects of recession, in accordance with Keynesian

economic thought. Similar policies have been adopted by other governments worldwide. This

is in stark contrast to the action permitted to Indonesia during its

financial crisis of 1997, when it was forced by the IMF to close 16

banks at the same time, prompting a bank run. Much

of the recent discussion reflected Keynes's advocacy of international

coordination of fiscal or monetary stimulus, and of international

economic institutions such as the International Monetary Fund and the World Bank, which many had argued should be reformed at a "new Bretton Woods" even before the crises broke out. IMF and United Nations economists advocated a coordinated international approach to fiscal stimulus. Donald

Markwel argued that in the absence of such an international approach,

there would be a risk of worsening international relations and possibly

even world war arising from similar economic factors to those present

during the depression of the 1930s. By

the end of December 2008, the Financial Times reported that "the sudden

resurgence of Keynesian policy is a stunning reversal of the orthodoxy

of the past several decades" In December 2008, Paul Krugman released his book, The Return of Depression Economics and the Crisis of 2008,

arguing that economic conditions similar to that which existed during

the earlier part of the century had returned, making Keynesian policy

prescriptions more relevant than ever. In February 2009 Shiller and

George Akerlof published Animal Spirits,

a book where they argue the current US stimulus package is too small as

it does not take into account Keynes's insight on the importance of

confidence and expectations in determining the future behaviour of

businessmen and other economic agents. In a March 2009 speech entitled Reform the International Monetary System, Zhou Xiaochuan, the governor of the People's Bank of China came

out in favour of Keynes's idea of a centrally managed global reserve

currency. Dr Zhou argued that it was unfortunate that part of the

reason for the Bretton Woods system breaking down was the failure to

adopt Keynes's Bancor. Dr Zhou proposed a gradual move towards increased used of IMF Special Drawing Rights (SDRs). Although Dr Zhou's ideas have not yet been broadly accepted, leaders meeting in April at the 2009 G-20 London summit agreed to allow $250 Billion of Special Drawing Rights to

be created by the IMF, to be distributed globally. Stimulus plans have

been credited for contributing to a better than expected economic

outlook by both the OECD and the IMF, in

reports published in June and July 2009. Both organizations warned

global leaders that recovery is likely to be slow, so counter

recessionary measures ought not be rolled back too early. While

the need for stimulus measures has been broadly accepted among policy

makers, there has been much debate over how to fund the spending. Some

leaders and institutions such as Angela Merkel and the European Central Bank have

expressed concern over the potential impact on inflation, national debt

and the risk that a too large stimulus will create an unsustainable

recovery. Among professional economists the revival of Keynesian

economics has been even more divisive with over 300 economists signing

a petition stating that they do not believe higher government spending

will help the United States's economy and some senior figures such as Robert Lucas remaining skeptical whether stimulus packages can work at all. Keynes's early romantic and sexual relationships were almost exclusively with men. Attitudes in the Bloomsbury Group, in which Keynes was avidly involved, were relaxed about homosexuality. One of his great loves was the artist Duncan Grant, whom he met in 1908, and he was also involved with the writer Lytton Strachey. Keynes

was open about his homosexuality, and between 1901 to 1915, kept

separate diaries in which he tabulated his sexual relationships. In 1921 he fell "very much in love" with Lydia Lopokova, a well-known Russian ballerina, and one of the stars of Serge Diaghilev's Ballets Russes. They married in 1925, leading to the widely repeated couplet of

unknown authorship: "Oh what a marriage of beauty and brains. The fair

Lopokova and John Maynard Keynes". Their union was by all accounts

happy, though

childless – Lydia became pregnant in 1927 but miscarried. For the first

years of the relationship, Keynes had maintained an affair with a

younger man, Sebastian Sprott, in tandem with Lopokova, but he

eventually chose Lopokova exclusively on marrying her. Among

Keynes' Bloomsbury friends, Lepokova was, at least initially, subjected

to criticism for her manners, mode of conversation and supposedly

humble social origins - the latter of the causes being particularly

noted in the letters of Vanessa and Clive Bell, and Virginia Woolf. E.M. Forster would later write in contrition: 'How we all used to underestimate her'. Keynes was ultimately a successful investor, building up a substantial private fortune. He was nearly wiped out following the Stock Market Crash of

1929 which he failed to foresee, but he soon recouped his fortune. At

his death in 1946 Keynes's worth stood just short of £500,000 -

equivalent to about £11 million ($16.5 million) in 2009. The sum

had been amassed despite lavish support for various good causes and his

personal ethics which made him reluctant to sell on a falling market as

he knew if too many did that it could deepen a slump. Keynes built up a significant collection of fine art, including works by Paul Cézanne, Edgar Degas, Amadeo Modigliani, Georges Braque, Picasso, and Georges-Pierre Seurat. He enjoyed collecting books: for example, he collected and protected many of Isaac Newton's papers. It is in part on the basis of these papers that Keynes wrote of

Newton as "the last alchemist." He was interested in literature in

general and drama in particular and supported the Cambridge Arts Theatre financially, which allowed the institution, at least for a while, to become a major British stage outside of London. Like several other notable British authors of his time, Keynes was a member of the Bloomsbury Group. Keynes was a life-long member of the Liberal party,

which until the 1920s had been one of the two main political parties in

Great Britain, and as late as 1916 had often been the dominant power in

government. Keynes had helped campaign for the Liberals at elections

from as early as 1906, yet he always refused to run for office himself,

despite being asked to do so on three separate occasions in 1920. From

1926 when Lloyd George became leader of the Liberals, Keynes took a

major role in defining the party's economics policy, but by then the

Liberals had been displaced into third party status by the Labour party. Keynes's personal interest in Classical Opera and Dance led him to support the Royal Opera House at Covent Garden and the Ballet Company at Sadler's Wells.

During the War as a member of CEMA (Council for the Encouragement of

Music and the Arts) Keynes helped secure government funds to maintain

both companies while their venues were shut. Following the War Keynes

was instrumental in establishing the Arts Council of Great Britain and

was the founding Chairman in 1946. Unsurprisingly from the start the

two organisations that received the largest grant from the new body

were the Royal Opera House and Sadler's Wells. Keynes was a proponent of eugenics, having served as Director of the British Eugenics Society from

1937 to 1944. As late as 1946, before his death, Keynes declared

eugenics to be "the most important, significant and, I would add,

genuine branch of sociology which exists." Throughout

his life Keynes worked energetically for the benefit both of the public

and his friends – even when his health was poor he laboured to sort out

the finances of his old college and to try to design an international monetary system that would benefit the whole world at Bretton Woods. Keynes suffered a series of heart attacks, which ultimately proved fatal, during negotiations for an Anglo-American loan in Savanna, Georgia, he was trying to secure on favourable terms for Great Britain from the United States, a process he described as "absolute hell". Keynes died of a heart attack at Tilton, his farmhouse home near Firle, East Sussex, on 21 April 1946 at age 62. It was a few weeks after returning from America. Both of Keynes's parents outlived him: father John Neville Keynes (1852–1949) by three years, and mother Florence Ada Keynes (1861–1958) by 12 years. Keynes's brother Sir Geoffrey Keynes (1887–1982) was a distinguished surgeon, scholar and bibliophile. His nephews include Richard Keynes (born 1919) a physiologist; and Quentin Keynes (1921–2003) an adventurer and bibliophile. His widow, Lydia Lopokova, lived on until 1981.